A failing reinforcement learning pipeline looks identical to a working one. The environment runs and the agent collects experience, but the reward curve stays flat and the policy collapses. The root cause is rarely the architecture; the issue is almost always the data.

In any RL time-series pipeline, data normalization matters more than network depth or reward shaping. It dictates what the agent actually sees. Feed it poorly scaled data, and the training fails regardless of compute. Normalize it correctly, and a minimal model is often enough to learn profitable behavior.

We isolate the effect by using a strictly minimal setup. The environment is a synthetic dataset with a repeatable pattern, solved by a small MLP+CNN policy. We default to PPO purely as a standard workhorse, but the lesson is universal: poorly scaled inputs break DQN, A2C, SAC, and other value-based methods in exactly the same way.

You can read endless papers on RL math and architecture, but making an agent actually learn often comes down to one mundane preprocessing decision that rarely makes it into the abstract.

We demonstrate how the exact choice of normalization dictates whether the model converges or collapses. Instead of abstract theory, we use concrete code and two side-by-side experiments to contrast z-score against percent-change.

Chapter 1: Creating the Synthetic Dataset

To train a reinforcement learning agent effectively, we need a dataset that allows the model to learn. This sounds trivial, but in practice, most real-world financial data is noisy, chaotic, and often lacks clear, repeatable signals — especially when starting with a minimal setup like a single "close" price time series.

Debugging a failed training run on real data is a nightmare because you cannot cleanly separate architecture flaws from normalization errors. We bypass this ambiguity by stripping the environment down to a deterministic synthetic series. Any basic model will find the pattern, provided the inputs are scaled in a way the network can actually process.

In this first step, we generate a fully synthetic time series that simulates a year of hourly close prices.

"""Generate synthetic financial close price data with repeatable patterns

for training reinforcement learning models."""

import random

import matplotlib.pyplot as plt

import pandas as pd

import numpy as np

# Setup: define time range and initialize close price array

NUM_HOURS = 8064

start_time = pd.Timestamp("2024-01-01 00:00:00")

time_index = pd.date_range(start=start_time, periods=NUM_HOURS, freq="h")

close = np.zeros(NUM_HOURS)

# Set starting close price

close[0] = 100.0

# Create random number generator (for reproducibility)

rng = np.random.default_rng(seed=42)

# Inject daily repeatable pattern every day at 10:00

pattern_indices = []

for day in range(NUM_HOURS // 24):

base = day * 24 + 10

if base + 5 < NUM_HOURS:

pattern_indices.append(base)

# Generate close prices with random variation and inserted patterns

i = 1

while i < NUM_HOURS:

if i in pattern_indices:

# Create upward trend for 5 hours (+0.3% per hour)

for j in range(5):

if i >= NUM_HOURS:

break

close[i] = close[i - 1] * 1.003

i += 1

# Sharp drop of -1.5% after the upward pattern

if i < NUM_HOURS:

close[i] = close[i - 1] * 0.985

i += 1

else:

# Otherwise apply random walk with small variation

delta = random.uniform(-0.002, 0.002)

close[i] = close[i - 1] * (1 + delta)

i += 1

# Save to CSV for further processing

df = pd.DataFrame(data={"close": close}, index=time_index)

df.to_csv("synthetic_close_data.csv")

# Plot the synthetic close prices

plt.figure(figsize=(12, 4))

plt.plot(close, label="Close Price", linewidth=1)

plt.title("Synthetic Close Price Time Series")

plt.xlabel("Time Step (hour)")

plt.ylabel("Close Price")

plt.grid(True, linestyle="--", alpha=0.5)

plt.legend()

plt.tight_layout()

plt.show()

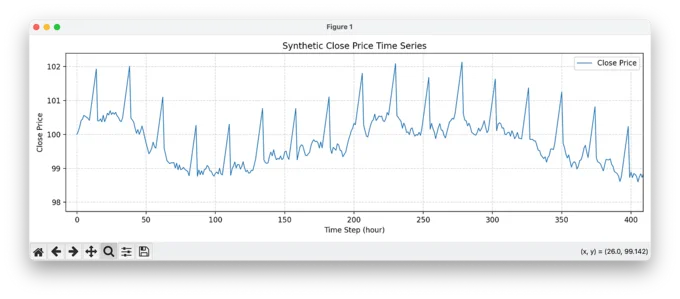

The core idea behind the code is simple: we inject a repeatable, tradable pattern every 24 hours. Specifically, at the same time each day (10:00), the synthetic price begins a 5-hour upward trend (+0.3% per hour), followed by a sharp drop of -1.5%. The rest of the time, the price behaves like a random walk with slight fluctuations (±0.2%).

This deterministic pattern is intentionally easy to exploit — if the model can't learn this, it certainly won't learn more subtle patterns in real financial markets. The simplicity allows us to focus on core mechanics like data normalization, reward shaping, and model behavior without being distracted by market noise.

The result is a clean training environment where we can observe whether the agent detects and acts upon the embedded opportunity. In the chart above, you can clearly see the repeated price ramps and drops — the signature our model should learn to trade. This visual confirmation gives us a solid baseline before we move on to more complex scenarios.

Chapter 2: We Need a Training Environment

Before we dive into real-world data or advanced strategies, we need one thing first: a stable and understandable training environment. In this project, the focus is not on building complex Gym wrappers or experimenting with exotic model architectures — we focus on the data and the reward function, because that's what really drives learning in reinforcement learning (RL) setups.

There are countless tutorials on how to set up a PPO environment using OpenAI Gym or Gymnasium. If you're reading this, chances are you've already seen some of them. So we'll keep it simple and skip the boilerplate.

We use Stable Baselines3 (SB3) because it's reliable, readable, and beginner-friendly. Sure, it's not perfect — scaling beyond a single machine is limited, and you'll hit walls eventually if you want distributed training. But for experimentation, debugging, and fast iteration, it's hard to beat. Rewriting everything in raw PyTorch, using RLlib or PyTorchRL, is massive overkill at this stage. You don't want to debug your framework before you debug your idea.

To improve the training quality, we use Maskable PPO, a variant of PPO that supports action masking. This means the model learns faster and more efficiently by being told in each step which actions are even valid. In our case, the action space is very simple — 4 discrete actions:

0: open a short position1: hold2: open a long position3: close an open position

def _get_action_mask(self):

mask = np.array([0, 1, 0, 0], dtype=np.int8)

if self.position == 0:

mask[0] = 1 # short

mask[2] = 1 # long

else:

mask[3] = 1 # close

return mask

Only some of these actions are allowed depending on the current position — e.g., you can't "close" if there's no trade open. Action masking helps the model avoid wasting learning capacity on invalid actions, and this has a huge impact on learning speed and stability.

The agent is trained using a small and simple MLP: two layers with 128 and 64 units. But — and this is crucial — we don't feed it raw flat input. We use a 1D Convolutional Neural Network (CNN) to extract features from the time series window. This gives us temporal pattern recognition without needing an LSTM or Transformer. We also include a small feedforward network for context input — specifically, the current position (long, short, or flat). The combined output is then passed into the MLP for action prediction.

This hybrid approach gives us the power of sequence modeling (via CNN) and context awareness (via a tiny context net), without the overhead or complexity of recurrent or attention-based architectures. It's fast, clean, and absolutely sufficient to prove that a pattern can be learned.

model = MaskablePPO(

policy=TradingPolicy,

env=train_env,

gamma=0.98,

clip_range=0.1,

n_epochs=10,

batch_size=64,

normalize_advantage=True,

learning_rate=1e-4,

tensorboard_log="tensorboard_exam/",

policy_kwargs=dict(

activation_fn=torch.nn.ReLU,

net_arch=[128, 64],

context_input_dim=1,

cnn_out_channels=64,

cnn_kernel_size=5,

),

verbose=1

)

In addition to defining the policy_kwargs when instantiating the model, it's important to note that both the feature extractor and the custom trading policy must be implemented manually. If you're interested in the full training setup or want to see the exact environment implementation, feel free to reach out — I'm happy to share more details. I've intentionally left out the boilerplate here to keep the focus on what's essential.

In short: we're not trying to build the perfect pipeline. We're trying to build something that works — and that lets us isolate the real questions: Did the model learn something useful? Did normalization help? That's what comes next.

Chapter 3: The Reward Function

If reinforcement learning is about learning through experience, then the reward function is the teacher. It tells the agent whether its actions were good, bad, or irrelevant — and in doing so, it shapes everything the model learns.

In our setup, the reward function is intentionally simple, but incredibly effective for the task at hand. It's embedded inside the step() method of our custom trading environment, and it governs how the agent is rewarded or penalized for taking actions like going long, going short, holding, or closing a position.

def step(self, act):

price = self.price[self.ptr]

reward = 0.0

if act == 2: # long

if self.position == 0:

self.position = 1

self.entry_price = price

elif act == 0: # short

if self.position == 0:

self.position = -1

self.entry_price = price

elif act == 3: # close

if self.position != 0:

if self.position == 1:

pnl = (price - self.entry_price) / self.entry_price

else: # short

pnl = (self.entry_price - price) / self.entry_price

reward = pnl

self.position = 0

self.entry_price = 0.0

elif act == 1: # hold

if self.position != 0:

pnl = (price - self.entry_price) / self.entry_price * self.position

reward += pnl * 0.01

self.ptr += 1

done = self.ptr >= len(self.price) - 1

if done and self.position != 0:

if self.position == 1:

pnl = (price - self.entry_price) / self.entry_price

else:

pnl = (self.entry_price - price) / self.entry_price

reward += pnl

self.position = 0

self.entry_price = 0.0

info = {"action": act, "reward": reward}

return self._obs(), reward, done, False, info

Here's what it does, in essence:

- If the agent opens a long or short trade, it receives no immediate reward — the trade has just begun.

- If the agent closes a position, it receives the full profit or loss (PnL) of that trade, calculated as the percentage change in price since the entry.

- If the agent holds an open position, it receives a small scaled reward based on the unrealized PnL. This encourages it to let profitable trades run — but only when it makes sense.

- If the episode ends and a trade is still open, the environment forces a close, and the final PnL is rewarded.

This structure is simple but captures the essence of trading: the agent is encouraged to enter good positions and close them at the right time, while avoiding trades that lead to losses. The reward is sparse — but not too sparse. It's shaped just enough to help the model learn when to act and when to wait.

What makes this work is the synthetic data we designed earlier. The reward function is able to clearly reflect whether the model has learned to recognize the daily pattern we injected. If it does, we expect the following behavior:

- The agent opens a long position right at the beginning of the pattern (around 10:00).

- It holds during the upward price movement.

- It closes before the sharp drop and opens a short position.

- It holds until the bottom is reached, then closes the trade.

- Everything else — in the best case, nothing. Just waiting for the next spike.

By designing a transparent reward function that aligns directly with the structure of the data, we remove a major source of uncertainty in RL training. Once this works, we can increase complexity — but only once we've proven that the fundamentals are solid.

Chapter 4 (Act I): Z-Score Normalization

We'll start our normalization journey with the classic: z-score normalization. It's simple, widely used, and — crucially — removes absolute price level effects so the model can focus on relative structure in the data.

# Z-Score Normalization

close = df_raw["close"]

close_norm = (close - close.mean()) / close.std()

df = pd.DataFrame({"close": close_norm}, index=close.index)

What it does

Z-score normalization centers the series at mean = 0 and rescales it so the standard deviation = 1 (approximately, up to floating error). That means:

- Price levels (e.g., 100 vs. 150 vs. 80) no longer matter.

- The daily synthetic spike pattern we injected earlier now shows up as structured positive deviations, followed by negative reversals, all in standardized units ("how many sigmas away from average").

- Background noise collapses into a tighter band around zero, making the spike pattern stand out more cleanly.

Tip: In production you normally compute mean/std on the training split only to avoid look-ahead bias. Here — in a fully synthetic, didactic setting — we normalize across the full dataset for clarity. We'll still evaluate on unseen splits to check generalization.

What the dataset looks like afterward

Instead of a drifting price curve, you now see a standardized oscillating series: long stretches near 0 with recurring multi-sigma moves where our +0.3% × 5-up / −1.5% drop pattern kicks in. These recurring excursions are exactly what we want the PPO agent to detect and trade. The normalization removes the distraction of absolute price scale so training can focus on shape.

Train/Val/Test splits to limit bias

We split the time series chronologically (e.g., 60% train / 20% validation / 20% test). The daily spike structure remains, but the levels and random walk noise between spikes differ in the validation and test portions. That matters: the model can't just memorize absolute values; it must respond to standardized moves.

We train the Maskable PPO agent for 500k steps on the z-score–normalized data.

The result: meh, not exactly great

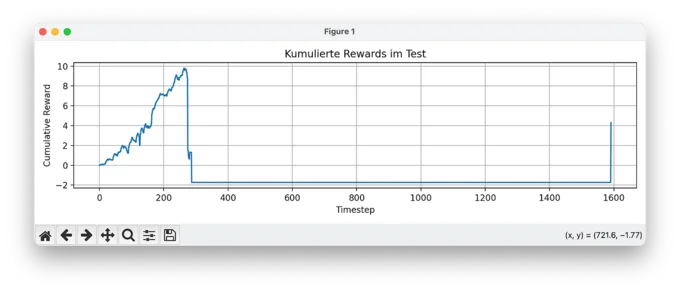

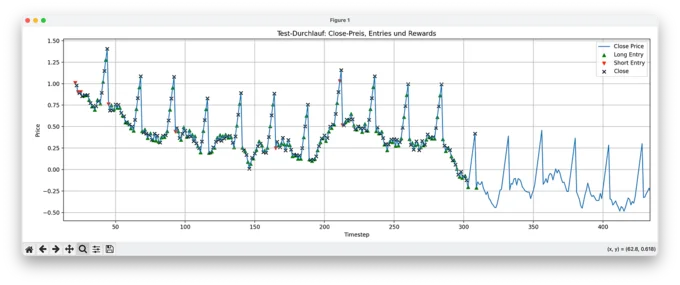

1. Cumulative Reward: The Collapse

At first glance, the training seemed to work: we see an early accumulation of rewards. But then, around timestep 300, everything falls apart. The model takes a series of bad trades and crashes into a negative reward zone, from which it never recovers. The agent continues through the episode without ever recovering, and barely trades at all. That's a sign that it completely lost signal — and confidence.

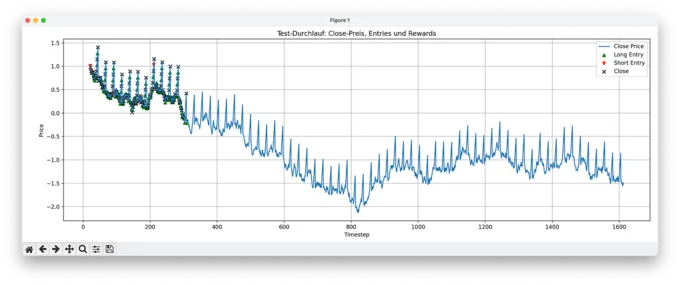

2. Test Overview: A Confused Start, Then Silence

Looking at the full test run, we see the agent trying both long and short positions early on. But its behavior is chaotic — entries seem random, closes are frequent but erratic. Once the price drifts far enough from the original z-score distribution (i.e. shifts too far in standardized terms), the agent completely stops trading. No action appears valid or rewarding anymore.

3. Zoom Detail: Nothing but Holds

Zooming in reveals what's happening: random long positions and after a certain point, the agent only executes hold actions. No entries, no closes — just passivity. This is a classic failure mode of PPO in poorly shaped environments: if the model can't connect its actions to positive rewards, it defaults to "do nothing" as the safest option.

Why this matters beyond PPO

This failure mode extends far beyond PPO. Whether you deploy DQN, SAC, or transformer-based actors, the network will collapse as soon as the input distribution shifts during evaluation. Applying Z-score normalization to absolute prices bakes the training distribution directly into the inputs. When test data drifts to new price levels, the standardized values enter a region the policy has never seen, breaking the learned mapping. Normalization does more than scale numbers; it defines whether an agent learns transferable logic or just memorizes a brittle set of absolute values.

Chapter 4 (Act II): % Normalization

In this part, we switch from z-score normalization of raw close prices to something more aligned with how financial time series behave: percent change normalization.

Instead of feeding absolute prices into the model (even normalized ones), we now work with percentage returns — the relative change from one timestep to the next. These percent changes are then themselves normalized (again via z-score) to ensure a consistent scale for learning:

# Percent-change + normalization for training, keep raw close for PnL

close = df_raw["close"]

pct_change = close.pct_change().fillna(0)

pct_norm = (pct_change - pct_change.mean()) / pct_change.std()

df = pd.DataFrame({

"close": close,

"feature": pct_norm

}, index=close.index)

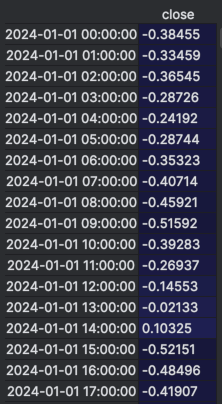

The screenshot below shows a raw excerpt from the dataset after applying percent-change normalization. The close column contains the original price, while the feature column shows the normalized percentage change used as input for training.

Even without any plotting, you can already see the daily pattern forming — look at the sequence starting from 2024-01-01 10:00:00 to 14:00:00. The feature values jump to 0.85651 consistently for several hours, which corresponds to our synthetic +0.3% per hour increase. Then, at 15:00:00, the sharp drop is reflected as a highly negative normalized value: -4.28747. That's our -1.5% cliff.

This table alone shows why percent-change normalization is so effective: the repeating spike pattern stands out clearly in the normalized feature column. It makes the job for the model (and for us) much easier — it no longer has to "guess" whether a move is big or small. Everything is standardized, and patterns become explicit.

Why this matters

With percent normalization, we're telling the model: "Don't learn based on price levels — learn based on how fast and in which direction things are moving."

This is a crucial mindset shift, and one that mirrors how most real-world trading models work. Markets behave in relative terms. A +1% move on a $10 stock is just as relevant as on a $1,000 stock. Price level ≠ signal.

Percent change is inherently stationary; absolute prices are not. Because the mean and variance of a percent-change series stay stable even when the underlying asset drifts arbitrarily, the agent receives a consistent input space. A ramp at price 100 looks mathematically identical to one at 150. The policy optimizes for the actual event, entirely decoupled from the current price level.

Visual clarity

You'll notice it immediately when plotting the normalized data: the spike pattern becomes visually obvious. No more masking by price drift or trend. You can see the five consecutive +0.3% moves, and the following -1.5% drop, now standardized and clean. The recurring wave is no longer buried in scale — it's front and center. Compared to the z-score normalized close prices, which still carry embedded structure from absolute levels, this version reveals the pattern much more clearly. The model benefits from that too.

Training with this representation

Just like before, we train our agent with 500,000 steps. The key difference is:

- We still retain the original close values in the dataframe.

- But these are not used during training — only for computing profit and loss (PnL) when trades are opened and closed.

This setup reflects a clean separation of observation (what the agent sees) vs. outcome (what defines reward). The model trains on normalized percent changes, but reward is always calculated in real money terms using actual price differences.

A strict separation between observations and rewards is fundamental for time-series RL. The observation space must exclusively contain stationary signals that allow generalization, such as returns, volatility ratios, or relative spreads. The reward function, however, must operate in absolute, real-world units like dollars or latency. If an agent is trained on normalized rewards, it will inevitably optimize the wrong objective.

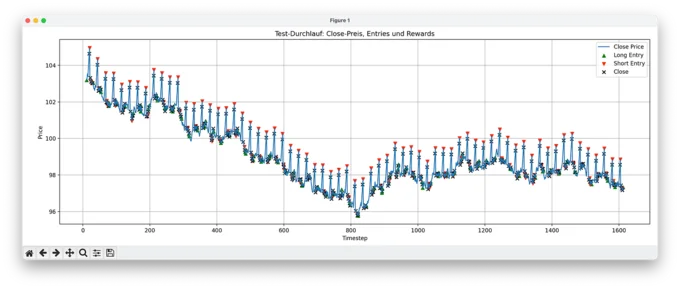

The result: it works

1. Full Test Set: Model Actions

In this plot, we see the model's predicted actions over the full test set. Despite the drifting and volatile price levels, the model opens trades precisely at the right moments: entering long before upward spikes, short before downturns, and consistently closing positions in time. The fact that it performs this well without access to price level information confirms that the normalization worked and the pattern was learned.

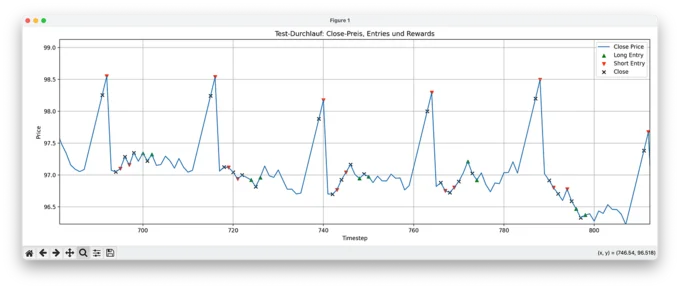

2. Zoomed-In View: Action Detail

Zooming in, we can observe individual long and short entries with their corresponding closes. The behavior isn't perfectly deterministic (nor should it be with PPO), but it's consistent and robust. The model has clearly learned to anticipate the repeating spike pattern and makes mostly profitable decisions.

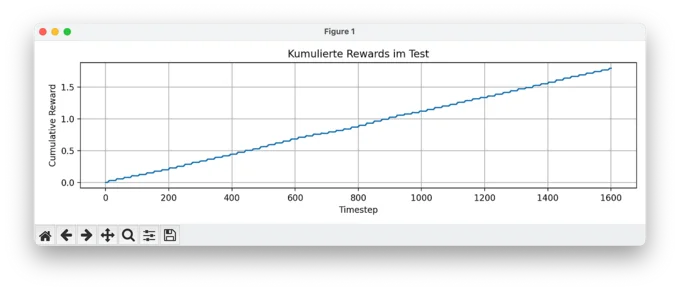

3. Cumulative Reward Over Time

Lastly, the cumulative reward plot shows exactly what we hoped for: a smooth, stable increase without drawdowns. No sudden losses, no reward volatility — just a clean reward curve that confirms the model is making good trades, over and over.

Conclusion

Two experiments with the exact same architecture, reward function, and algorithm produced radically different outcomes. Z-score normalization on absolute prices led to policy collapse, while percent-change normalization enabled smooth convergence. The only variable was the observation space.

This principle applies to any time-series RL deployment, from financial markets to system telemetry. An agent simply learns the statistical structure of its inputs. If the observations encode a non-stationary signal, like absolute prices or drifting baselines, the policy couples to a distribution that will break in production. If the observations are stationary, the policy generalizes.

The operational rule is strict: before modifying the network or tuning the reward, audit your observation space. Plot the distributions of your training and test splits. If they don't match, you are forcing the agent to extrapolate, not to learn. Production RL failures frequently masquerade as complex algorithm deficits, but they are almost always observation-space mismatches — fixable with precise data preprocessing.